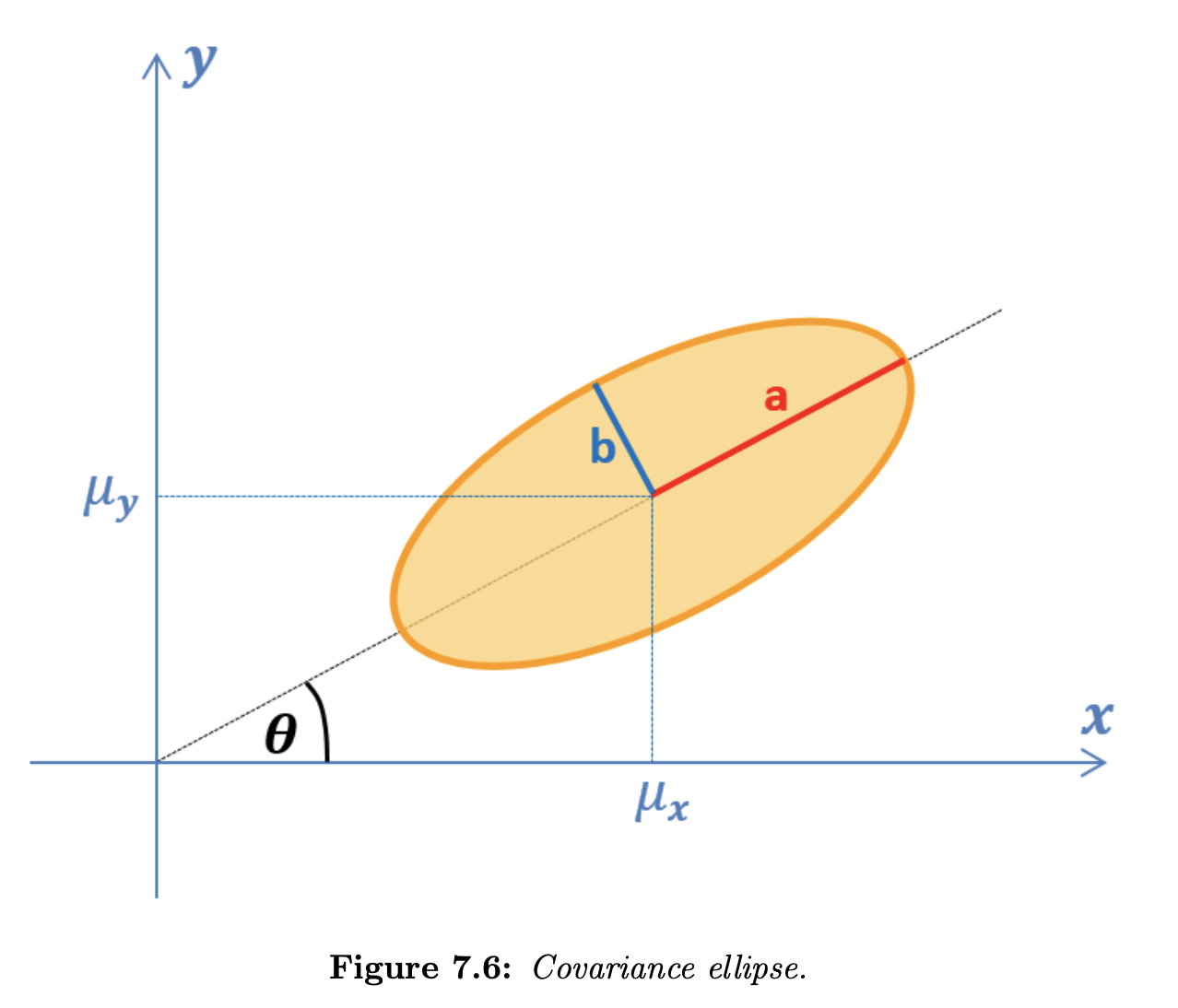

First, let us find the properties of the covariance ellipse of a bivariate distribution. The covariance ellipse represents an iso-contour of the Gaussian distribution and allows visualization of a confidence interval in two dimensions. The covariance ellipse provides a geometric interpretation of the covariance matrix.

Any ellipse can be described in four parts:

- Ellipse center

- Half-major axis

- Half-minor axis

- Orientation angle

The ellipse center is a mean of the random variable:

The lengths of the ellipse axes are the square roots of the eigenvalues of the random variable covariance matrix:

- The length of the half-major axis is given by the highest eigenvalue square root

- The length of the half-minor axis is given by the second eigenvalue square root

The orientation of the ellipse is an orientation of the covariance matrix eigenvector that corresponds to the highest eigenvalue:

where:

- is the -coordinate of the eigenvector that corresponds to the highest eigenvalue

- is the -coordinate of the eigenvector that corresponds to the highest eigenvalue

Python example:

import numpy as np

C = np.array ([[5 , -2] ,[ -2 , 1]]) # define covariance matrix

eigVal , eigVec = np.linalg.eig(C) # find eigenvalues and eigenvectors

a = np.sqrt (eigVal [0]) # half - major axis length

b = np.sqrt (eigVal [1]) # half - minor axis length

# ellipse orientation angle

theta = np.arctan (eigVec [1 , 0] / eigVec [0 , 0])