A covariance matrix is a square matrix that represents that covariance between each pair of elements in a given multivariate random variable.

For a 2D random variable, the covariance matrix is

The off-diagonal entries are equal since . If and are uncorrelated, the off-diagonal entries of the covariance matrix are zero.

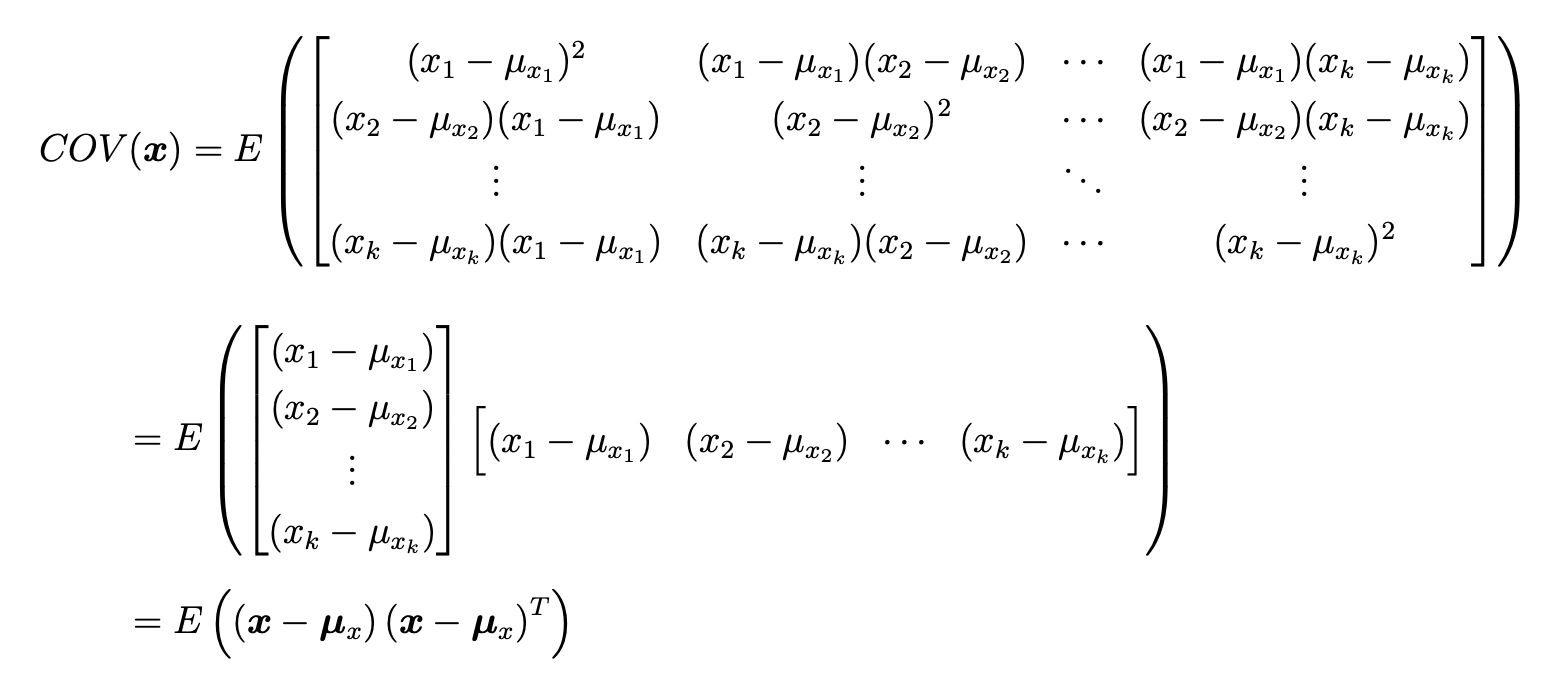

For a -dimensional random variable, the covariance matrix is given by

Properties

- The diagonal entries of the covariance matrix are the variances of the components of the multivariate random variable.

- Since the diagonal entries are all non-negative, the trace (sum of diagonal entries) is also non-negative:

- Since , the covariance matrix is symmetric:

- The covariance matrix is positive semidefinite. The matrix is called positive semidefinite if for any vector . The eigenvalues of are non-negative.

Covariance Matrix and Expectation

Assume a vector with elements:

The covariance matrix of the vector is

where is the mean of the random variable.